Prior Authorization Explained: How It Works And What To Do

Every year, physicians submit roughly 100 prior authorization requests per week on average, according to the American Medical Association, and each one takes time away from patient care. If you've ever had a doctor tell you that your insurance needs to "approve" a procedure or medication before you can get it, you've already encountered prior authorization explained in its most frustrating form.

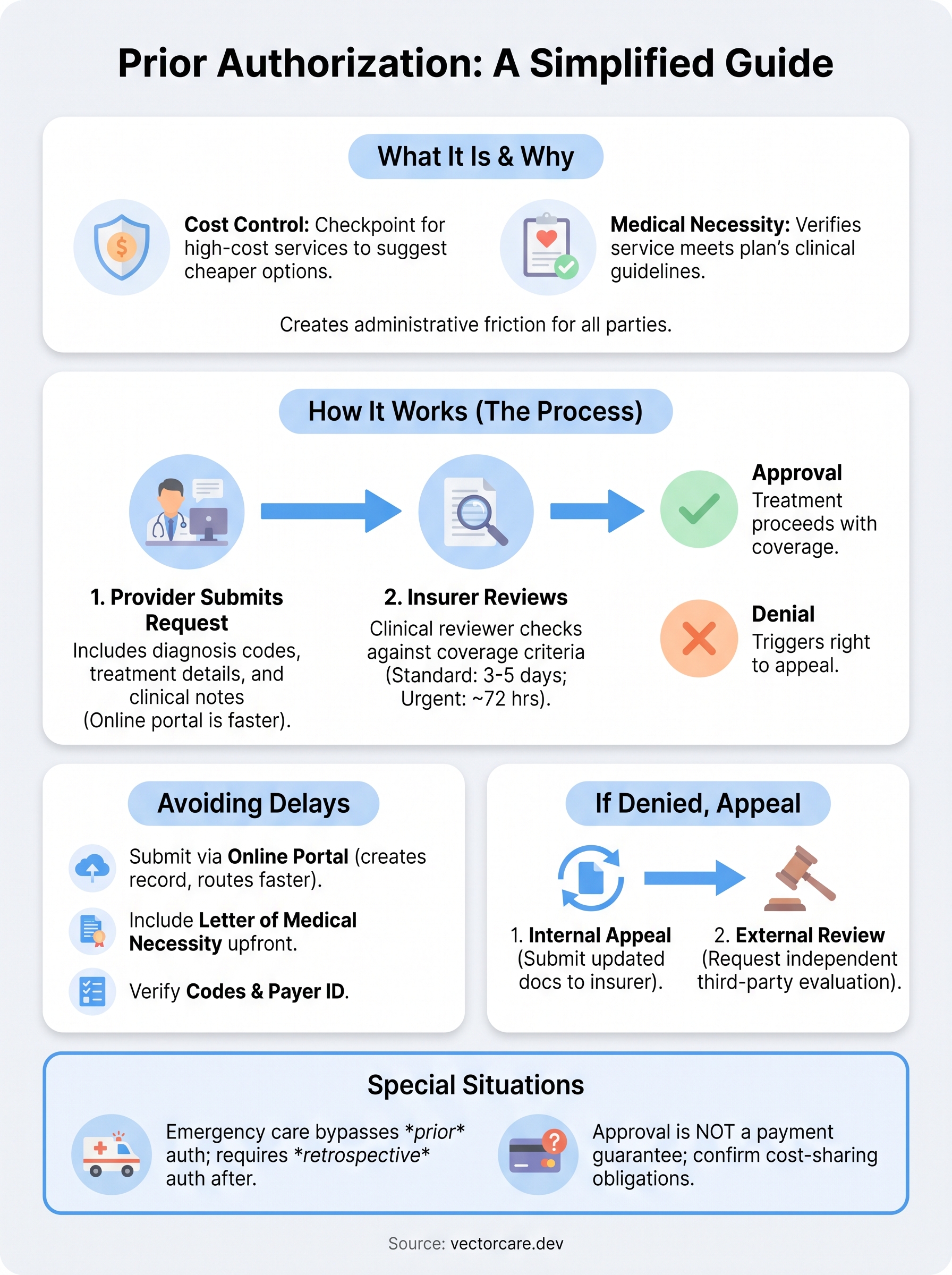

Prior authorization is the process where a health insurance company requires advance approval before it will cover a specific treatment, medication, or service. It exists to control costs and verify medical necessity, but it also creates significant administrative friction for providers, vendors, and patients. For healthcare vendors building tools that touch clinical workflows, especially those integrating with EHR systems like EPIC, understanding how prior authorization works is essential to designing solutions that actually reduce this burden rather than add to it. That's a core reason platforms like VectorCare Dev SoFaaS exist: to help vendors embed prior auth and other workflows directly into EPIC without building from scratch.

This article breaks down what prior authorization is, why insurers require it, how the approval process works step by step, and what you can do when a request gets denied.

Why health plans require prior authorization

Health plans use prior authorization as a utilization management tool to control what gets covered and when. The core idea is that not every treatment a physician orders is automatically the most cost-effective or clinically appropriate option, and insurers want a checkpoint to review high-cost or potentially overused services before they approve payment. Two primary motivations drive the requirement: controlling costs and enforcing medical necessity standards.

Cost control is the primary driver

Insurers are running a financial operation, and prior authorization requirements concentrate heavily on treatments that carry significant price tags. Brand-name drugs with cheaper generic alternatives, advanced imaging like MRIs and CT scans, elective surgeries, and specialty care referrals are all frequent targets. When a health plan routes these through a pre-approval process, it creates a checkpoint where a less expensive alternative can be suggested or required before the higher-cost option gets covered.

According to the American Medical Association's 2023 Prior Authorization Physician Survey, 94% of physicians reported that prior authorization delays access to necessary care.

Payers also use authorization data to identify patterns of overutilization across their provider networks. If a specific provider orders a test at a much higher rate than peers, the prior auth process gives the insurer visibility into those patterns and a lever to push back before costs accumulate.

Medical necessity is the stated standard

The second reason health plans require prior authorization is to verify that a requested service meets their medical necessity criteria. Every insurer maintains clinical guidelines, often built on third-party evidence-based resources, that define which conditions justify a specific treatment. If your physician requests a procedure that doesn't match those criteria based on your diagnosis codes and clinical documentation, the plan can deny coverage before any services are rendered.

This is where prior authorization explained in its simplest form becomes useful: the insurer is not deciding whether you need care, it's deciding whether it will pay for that specific care under your plan's terms. Understanding this distinction helps both patients and healthcare vendors design workflows that front-load the right clinical documentation, so requests clear the necessity review on the first submission rather than cycling through repeated back-and-forth with the payer.

How prior authorization works step by step

The prior authorization process follows a predictable sequence, and prior authorization explained at its most practical level is a three-step workflow between your provider and your insurer. Knowing each step helps you stay ahead of delays and submit requests that move through the review process without unnecessary back-and-forth.

Step 1: Your provider submits the request

Your physician or their administrative staff initiates the process by sending a prior authorization request to your insurer. This submission typically includes your diagnosis codes, the specific treatment or medication being requested, and supporting clinical notes that justify medical necessity. Most payers accept requests by fax, phone, or through an online portal, and portal-based submissions generally process faster.

Step 2: The insurer reviews for medical necessity

Once the payer receives the request, a clinical reviewer checks whether the service meets the plan's coverage criteria. For standard requests, most insurers must respond within 3 to 5 business days. For urgent cases, a 72-hour turnaround is common under federal guidelines for managed care plans.

The Centers for Medicare & Medicaid Services requires Medicare Advantage plans to respond to standard prior authorization requests within 7 calendar days.

Step 3: You receive an approval or denial

After the review is complete, the insurer notifies both you and your provider of the decision. An approval clears the way for the treatment to proceed with coverage. A denial triggers your right to appeal, and you should act on that quickly since most plans set strict deadlines for submitting one.

What delays prior authorization and how to speed it up

Prior authorization delays usually trace back to a small set of preventable errors in the initial submission. Understanding these common failure points, with prior authorization explained at this operational level, gives you and your care team a real advantage in moving requests through the review queue faster.

Missing or incomplete documentation

The most common reason a request stalls is that the payer's clinical reviewer can't find enough supporting documentation to approve the service on the first review. Missing diagnosis codes, incomplete chart notes, or a lack of documented prior treatment attempts (known as step therapy requirements) all trigger a request for additional information, which can add days or even weeks to the process.

A second issue is a mismatch between the diagnosis code submitted and the payer's clinical criteria for that service. Even a minor coding error can send a request back to the provider for correction, restarting the clock entirely.

The American Medical Association's 2023 survey found that 94% of physicians reported that prior authorization sometimes, often, or always delays access to necessary care.

What you can do to move faster

Your best tool for speeding up a request is submitting through the insurer's online portal rather than fax or phone. Portal submissions create a time-stamped record, reduce manual handling errors, and route directly to the clinical reviewer queue. Ask your provider's office to attach a letter of medical necessity with every submission, even when the payer doesn't explicitly require one, because it directly addresses clinical criteria upfront.

A few additional steps that consistently reduce turnaround time:

- Confirm the correct payer portal ID or fax number before submitting

- Request an urgent review if the clinical situation qualifies

- Follow up by phone after 48 hours if you haven't received a status update

What to do if your prior authorization is denied

A denial is not the end of the road. With prior authorization explained at its most actionable level, a denial is the start of a formal review process that gives you and your provider specific rights to challenge the insurer's decision.

File an internal appeal first

Your first step is to request an internal appeal directly with your insurer. Most plans require you to submit this within 30 to 60 days of receiving the denial notice. Your provider should prepare an updated letter of medical necessity that directly addresses the reason the insurer cited for the denial, along with any additional clinical documentation that closes the gap.

Under the Affordable Care Act, insurers must complete an internal appeal review within 30 days for non-urgent services and 72 hours for urgent care situations.

Request an external review if the appeal fails

If the insurer upholds the denial after the internal appeal, you have the right to request an independent external review. An external reviewer is a third-party organization that evaluates whether the denial was medically appropriate under your plan's terms. This reviewer operates independently from your insurer, and its decision is binding on the plan.

Contact your state insurance commissioner's office if you're unsure how to initiate an external review, since state-specific rules vary on deadlines and filing procedures. Acting quickly after a failed internal appeal protects your access to this option before any filing window closes.

Common questions and special situations

With prior authorization explained across the main workflow, a few specific scenarios still catch patients and providers off guard. Knowing how insurers handle these edge cases helps you plan ahead and avoid coverage gaps when the standard process doesn't apply.

Does prior authorization guarantee payment?

Approval of a prior authorization request does not guarantee that your insurer will pay the final claim. The insurer still reviews the claim against your benefits, deductible, and any other plan terms after the service is rendered. Always confirm your cost-sharing obligations with the plan before you schedule a procedure, even after an authorization is approved.

A prior authorization approval confirms medical necessity but does not override your plan's coverage limits, exclusions, or cost-sharing requirements.

What about emergency situations?

Emergency care does not require prior authorization before you receive treatment. Federal law requires insurers to cover emergency services without advance approval, regardless of whether the provider is in-network. However, your insurer may still require retrospective authorization after the fact, which your provider typically handles on your behalf within a specific window, often 24 to 72 hours after admission.

Prior authorizations also have expiration dates, typically 60 to 90 days from the approval date. If your procedure gets delayed past that window, your provider must submit a new request. Check the expiration date on every approval letter so you don't lose coverage because the authorization lapsed before the appointment.

Key takeaways

Prior authorization explained at its core is a coverage checkpoint, not a final verdict on your care. Health plans require advance approval to verify medical necessity and control costs before paying for high-cost treatments, medications, or procedures. Knowing the process gives you a real advantage: submit complete documentation on the first request, confirm your payer's portal preferences, and track every approval's expiration date so coverage doesn't lapse before your appointment.

When a denial arrives, treat it as the start of a formal review process. File an internal appeal with updated clinical documentation, and request an independent external review if that appeal fails. Emergency care bypasses prior authorization, but your provider still needs to handle retrospective authorization quickly after treatment.

For healthcare vendors building tools that touch these workflows, embedding prior auth directly into clinical systems removes friction at every step. See how VectorCare Dev SoFaaS helps you integrate into EPIC without building from scratch.

The Future of Patient Logistics

Exploring the future of all things related to patient logistics, technology and how AI is going to re-shape the way we deliver care.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.